Hi, I'm

Senior UX Designer

I design onboarding, activation and payments for fintech and retail products used by millions. Most recently: taking thinkmoney customers from sign-up to first transaction in a single session, down from a 3-5 day wait.

Senior designer inside a live challenger bank. Virtual cards and Open Banking funding shipped as one journey, and the team learning to work faster with AI along the way.

A financial wellbeing platform built from nothing as founding designer: brand identity through to a live product on both app stores, with an AI guide grounded in behavioural science.

The core shopping journey on an app serving six million users: registration and onboarding, home, listings and product pages. I owned the flows from the first user interview through to build.

Senior UX designer with 8 years in design, most of them in fintech and retail. I work best where design sits close to the decisions, and I keep it there by staying close to the research.

Here are a few kind words people have to say about collaborating and solving problems with me.

Liam is exceptionally talented and is passionate about creating meaningful, accessible and desirable products for our users. He consistently demonstrates a profound understanding of user-centred design using design thinking to enhance the user’s journey and overall satisfaction.

Liam has owned the App project in which he has been the UX design lead. His eye for detail and positive attitude has ensured this project was delivered at high standards with tight timeframes. I can always count on Liam to deliver.

Liam works effectively with cross-functional teams and individually. He has strong problem-solving skills and creativity when faced with challenges. I am confident that Liam will excel in any role and wholeheartedly recommend him without hesitation.

I enjoyed working with, and managing, Liam. He’s really dedicated to getting the job done, giving each task his all and putting overtime in to get urgent work over the line. He’s passionate about self development too, which is always good to see.

A financial wellbeing platform blending AI guidance with gamified, behaviour-led design. As founding designer I took it from brand identity to a shipped product.

01 · The challenge

Source: figures cited at moneyappi’s launch (Workplace Journal, 2025); underlying data attributed to Deloitte and the Health and Safety Executive.

Yet most workplace financial benefits sit unused, because they feel bought for everyone and built for no one. Money anxiety bleeds into confidence, into productivity, into the decisions people make every day. And the tools that exist are either clinical or hard to stick with. Usually both.

moneyappi set out to change that. The experience I was hired to design had to help people genuinely understand their finances, without ever making them feel overwhelmed or judged.

moneyappi Ltd was incorporated on 1 August 2024, the month I joined as its first designer. The company sits within Think Money Group, the same group I later moved across to at thinkmoney, so this project is the first half of a two-year arc with one employer.

The first thing I changed was the name. The working concept was Money Wellness in Work, borrowed from Money Wellness, the group’s existing debt-solutions brand. I argued against it in my first weeks: a product asking employees to build financial confidence shouldn’t share a name with the service people turn to when things have already gone wrong. It would have framed the app as somewhere you go with problems rather than somewhere you go to make progress.

The concept became moneyappi. Welly became Buddi.

02 · Research & discovery

I tested early concepts with more than 20 participants using Figma prototypes and moderated sessions over Zoom and in person, primarily with HR professionals and general employees across mixed industries.

“Users who were already anxious about money found data-heavy interfaces made things worse, not better. They wanted to feel supported, not assessed.”

I also ran a separate research strand with HR professionals. What they needed was a clear story to take to senior leadership: proof the platform was working, and a reason to keep paying for it.

03 · Defining the experience

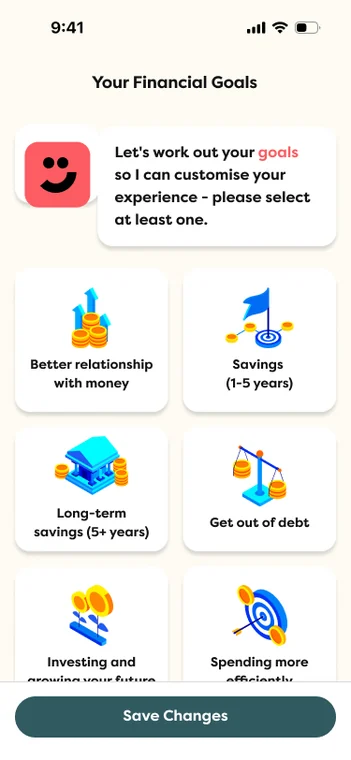

Working alongside behavioural scientists, the product was built around three principles: making financial wellbeing feel approachable, encouraging consistent small improvements, and creating visible progress that kept users coming back.

The behavioural science wasn’t window dressing. It set how habits were structured and how Buddi™ spoke to people, and the reward system followed the same rule: reinforce, never pressurise.

04 · Buddi™

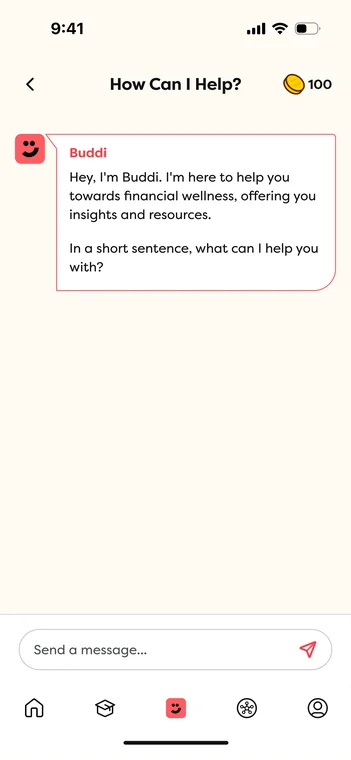

The hardest moment in any financial product is not knowing where to start. Buddi™ exists for that moment: a conversational, non-judgemental layer of guidance with two modes, plain-language Q&A and personalised nudges tied to the user’s own behaviour.

Buddi™ interactions consistently outperformed expectations in testing. Users didn’t just find it useful, they found it reassuring, which was the point.

Buddi™ guides goal-setting during onboarding and surfaces contextual nudges tied to real user behaviour throughout.

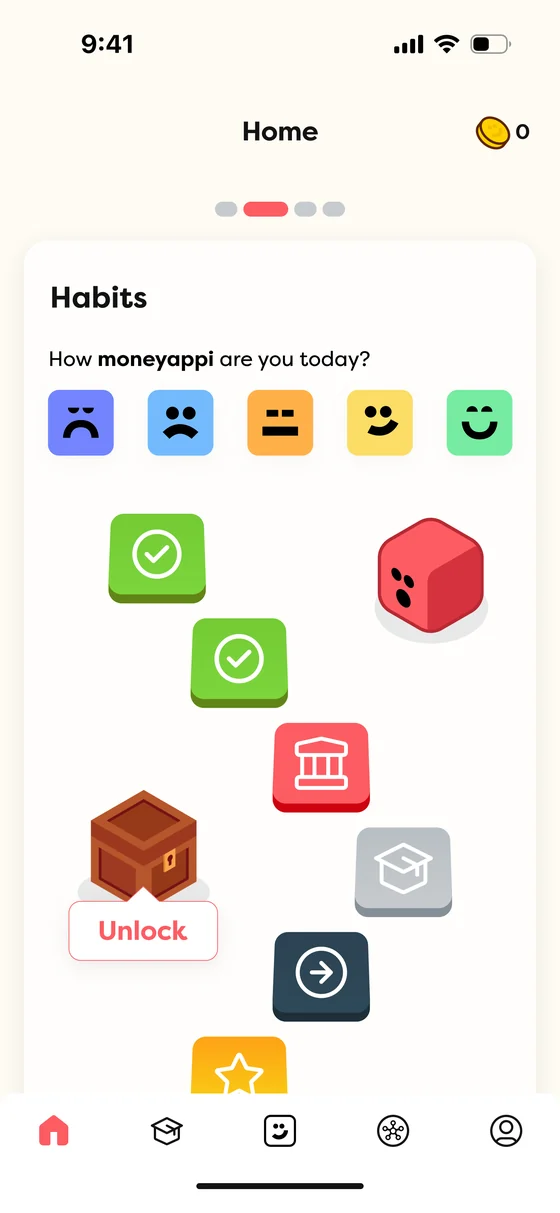

05 · Gamification & behavioural design

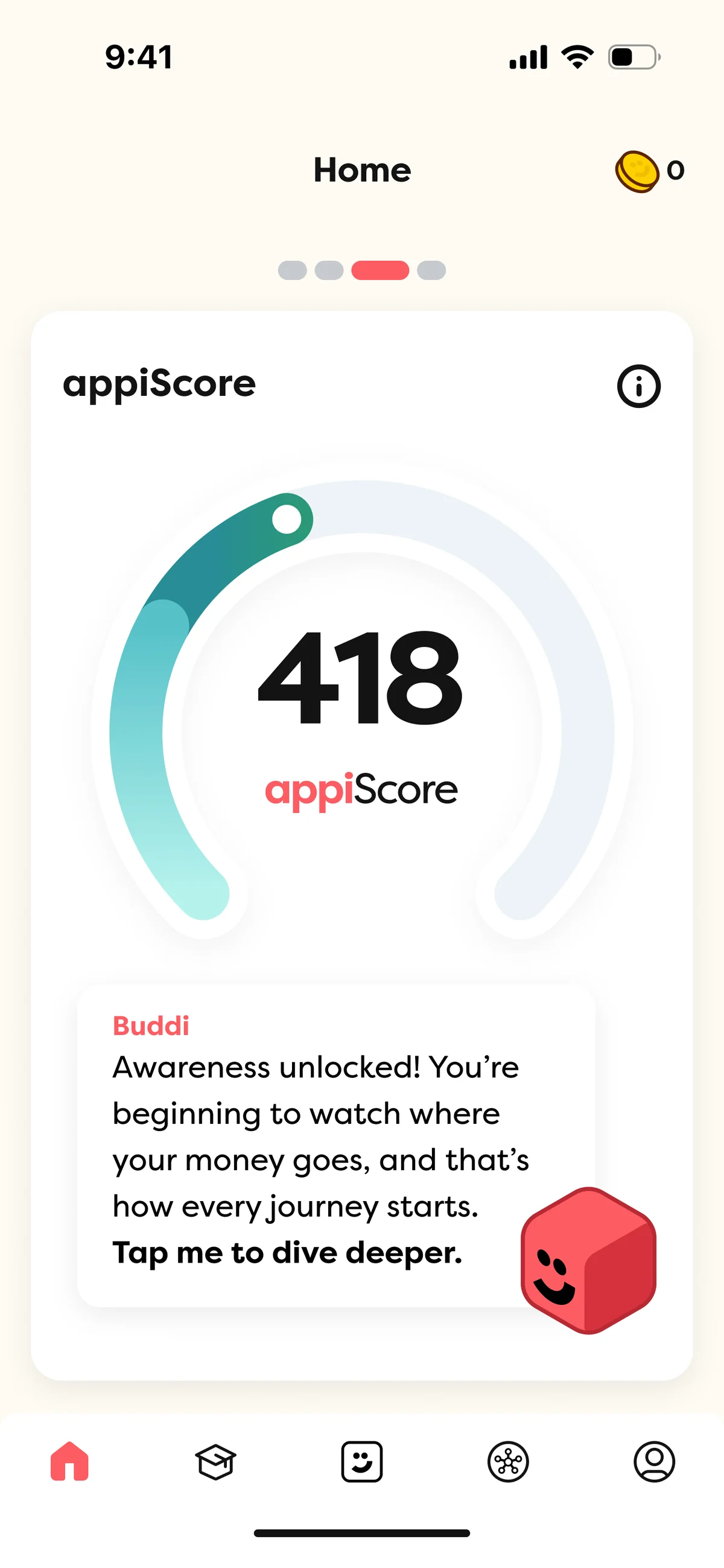

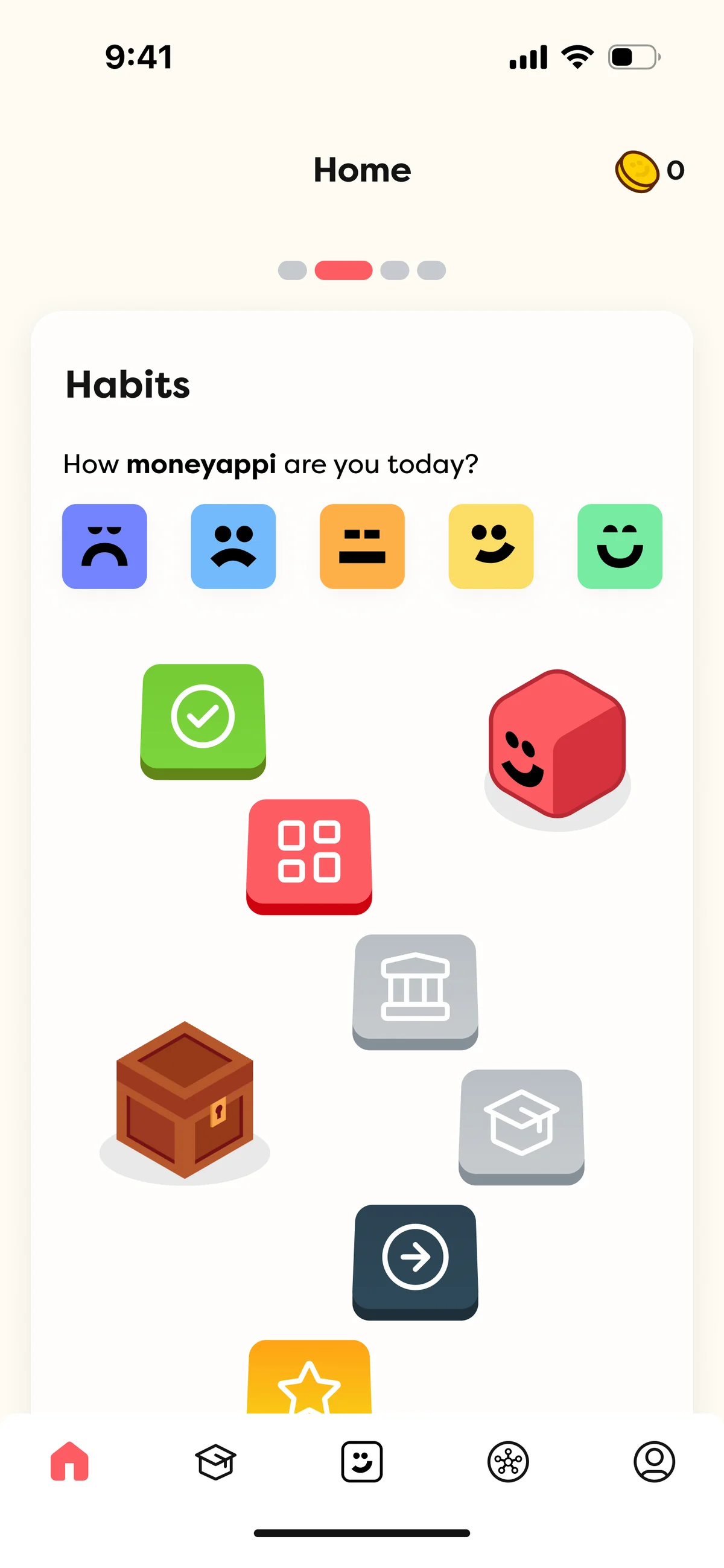

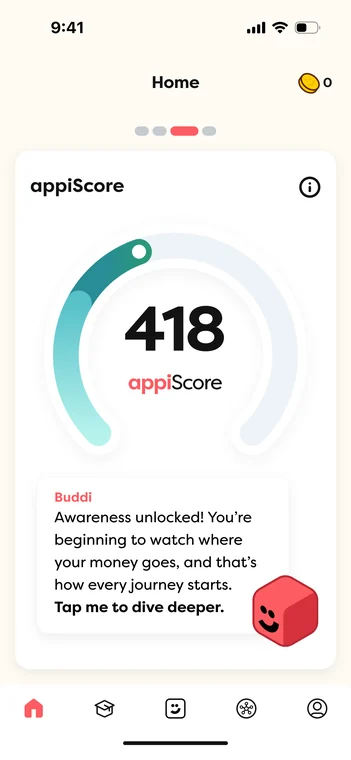

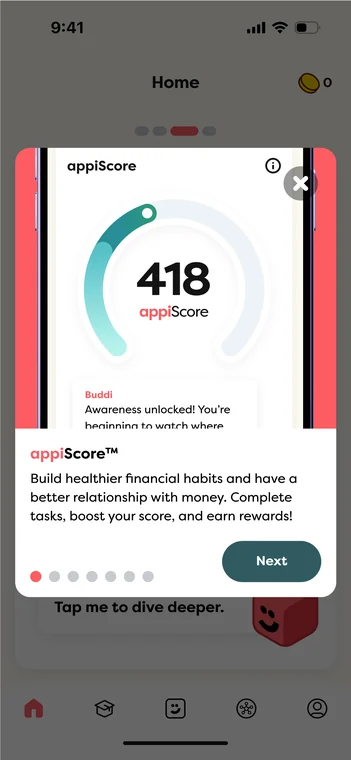

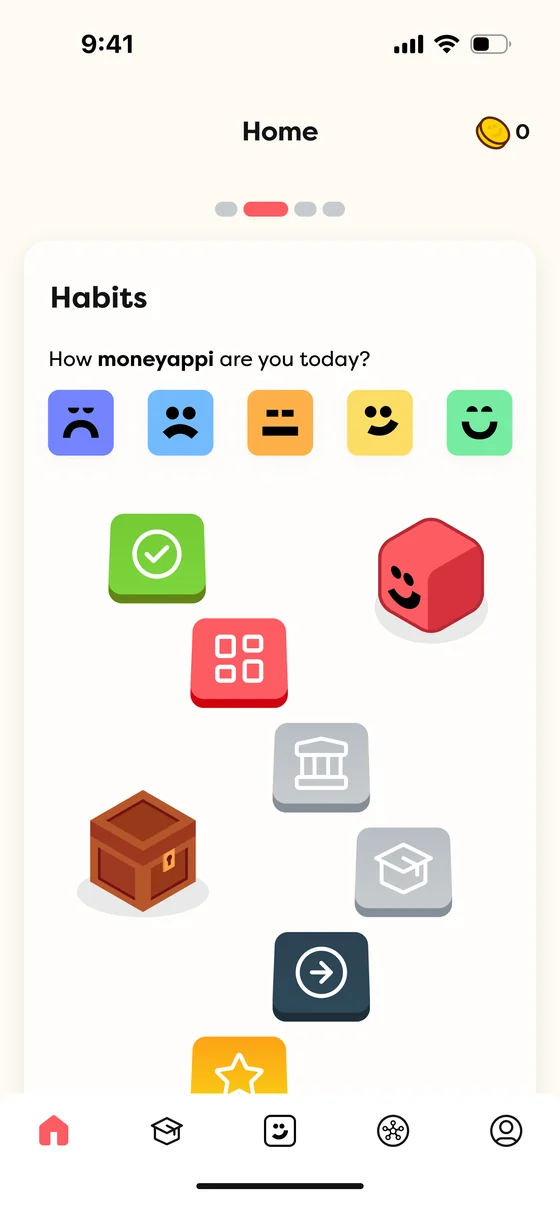

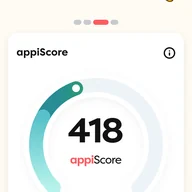

A persistent pattern in the research: people start well with financial apps, then quietly stop. So I designed for visible progress. Coins earned, habits completed, and an appiScore™ (the platform’s proprietary financial wellbeing score) that climbs as behaviour changes. That loop was the product.

The chest stays shut until a habit is completed. Buddi reacts when there’s something to open.

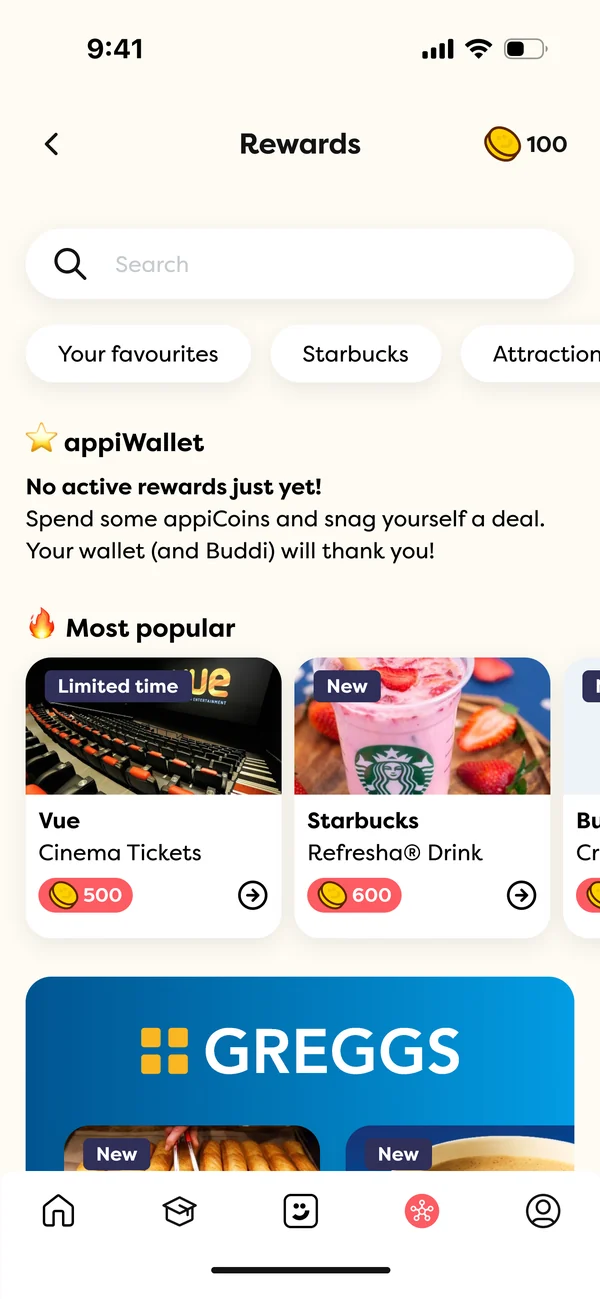

AppiCoins had to be worth something real, so the reward marketplace was backed by brands people actually use: Greggs, Starbucks, Vue and ASOS on the consumer side, with Reward Gateway, HubSpot, Notion and REBA as enterprise partners.

Coins earned through habits, spent on real rewards: the loop closes in the appiWallet.

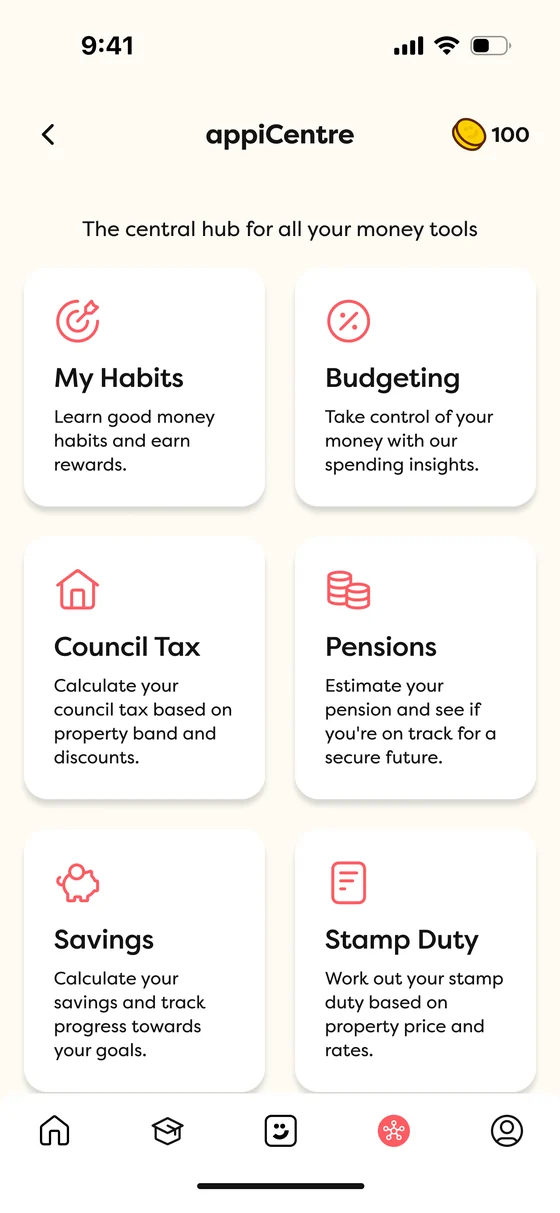

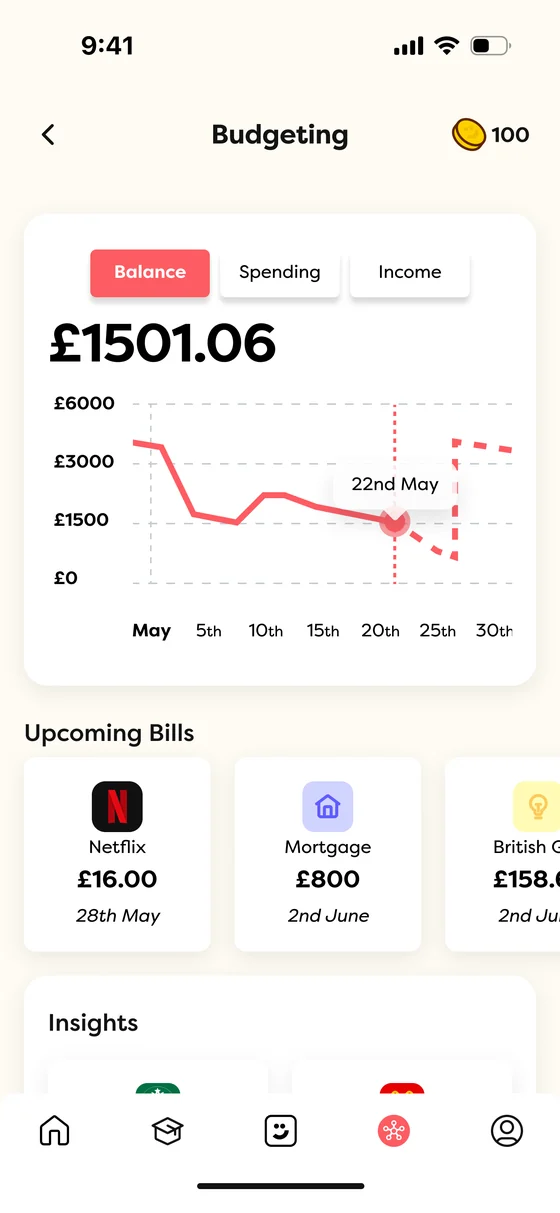

06 · appiCentre

When a platform has real functional depth, the risk is that users never find most of it. The appiCentre brought budgeting, habits, council tax, pensions, savings and stamp duty tools into a single hub. Breadth stayed visible without reading like a feature list.

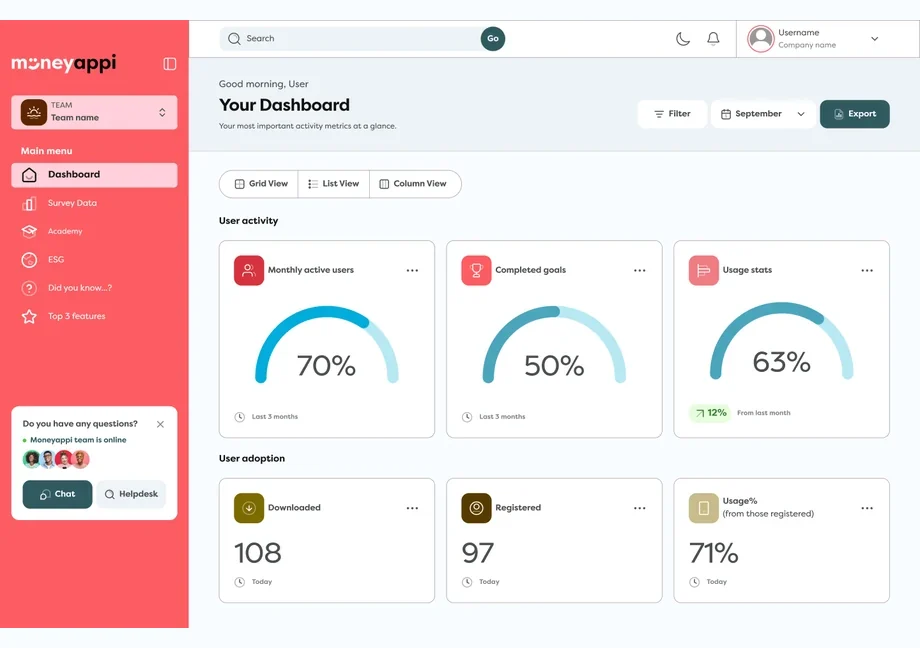

07 · HR dashboard

HR teams didn’t need more data. They needed something they could open five minutes before a leadership meeting and walk in confident. I centred the experience on the average appiScore dial, with supporting metrics and a prominent Export function that came straight out of the research.

The original lacked hierarchy and narrative. The redesign centres the average appiScore with exportable engagement metrics.

08 · Design & visual system

Financial services have a long history of designing for authority over accessibility. We consciously went the other way: a warm, digestible system whose visual cues reward progress instead of highlighting what’s missing.

09 · Outcomes & reflection

moneyappi launched publicly on iOS, Android and web, taken from brand identity through to a shipped product. It remains live and in active development, with the gamified progression model and appiScore established at launch still central to the product today.

“This project was never really about screens. It was about changing how people felt about their own financial lives.”

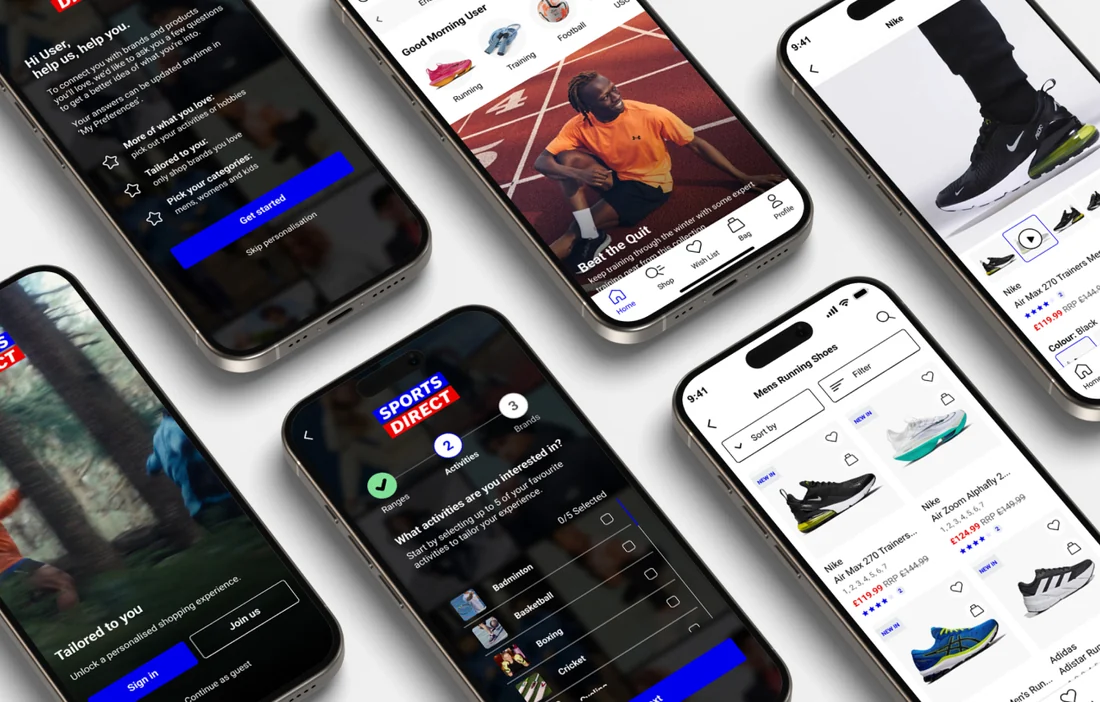

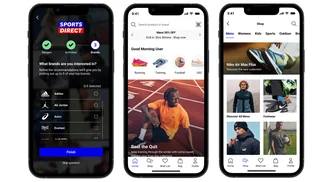

Lead UX on the Sports Direct app redesign. I designed the shopping experience end to end: registration, onboarding, home, product listing and product detail, on an app with 6.1 million users.

01 · Overview

Sports Direct set out to turn its app into a personalised shopping platform. As Lead UX Designer I designed the core shopping journey end to end: registration and onboarding, the home screen, product listings and product detail pages.

This case study goes deepest on registration and onboarding, because the whole ambition lived or died there: if people didn’t register or never finished onboarding, nothing downstream could be personalised. It is one part of the remit, not the whole of it.

The numbers

One baseline and two targets, set at kick-off. See Outcomes for what shipped and what was validated.

02 · Discovery

I started with the competition: four direct rivals and two indirect ones, examined purely through their registration and personalisation flows. Then I interviewed eight users, deliberately mixed in age, gender and experience of shopping online, to hear first-hand where sign-up loses people.

03 · Key insights

04 · Ideation

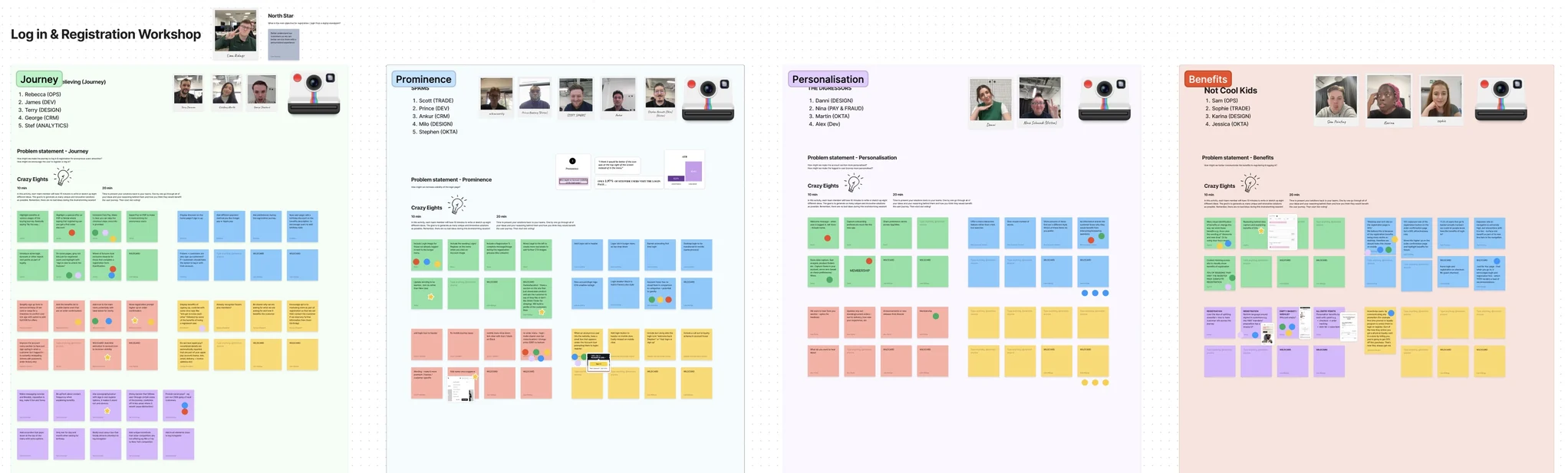

I facilitated an ideation workshop with four cross-functional teams, each assigned a problem statement from discovery: Journey, Prominence, Personalisation, and Benefits.

Takeaway: framing discovery findings as problem statements for four cross-functional teams built shared ownership of the solution before any design began.

“We focused on quantity over quality to foster open dialogue, voting on the most promising solutions to refine further.”

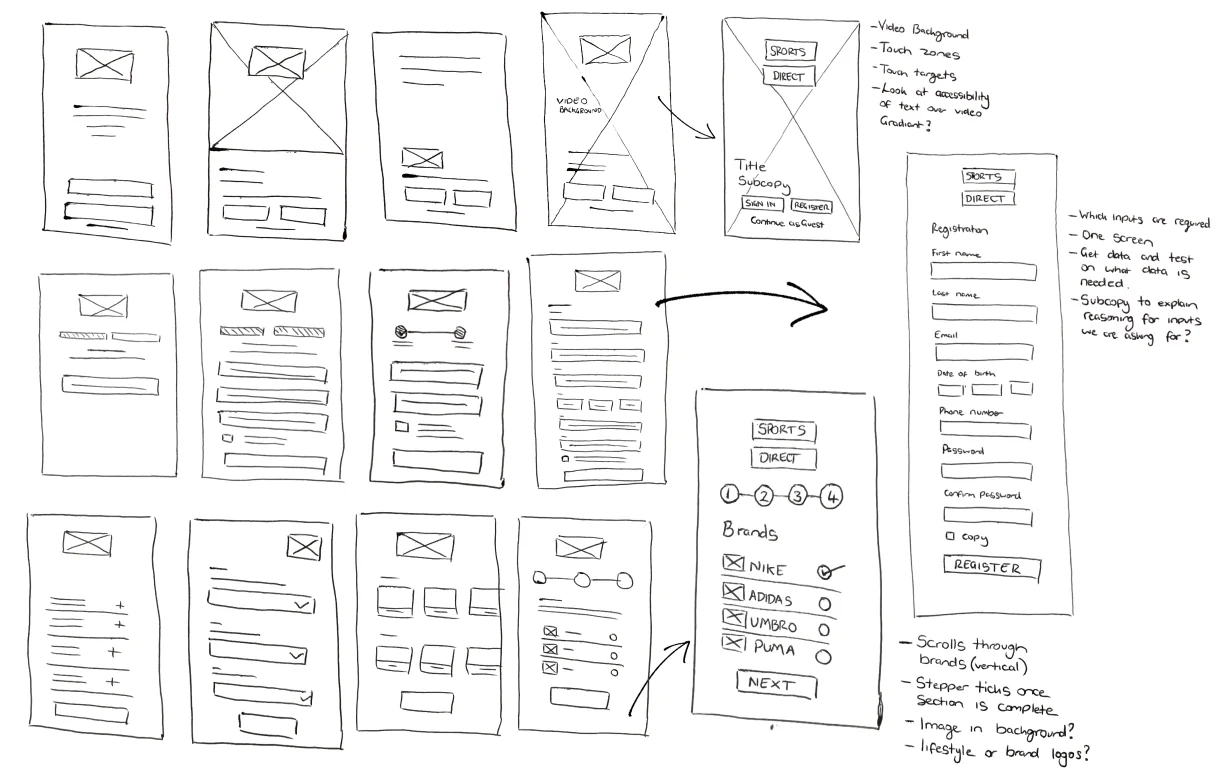

05 · Wireframing

The research and workshop outputs became wireframes: the first-run screen, registration, and a personalisation step that hadn’t existed in the app before. I iterated on them until they were worth putting in front of users.

Wireframes for the first-run screen, registration and the new personalisation onboarding step, refined before testing.

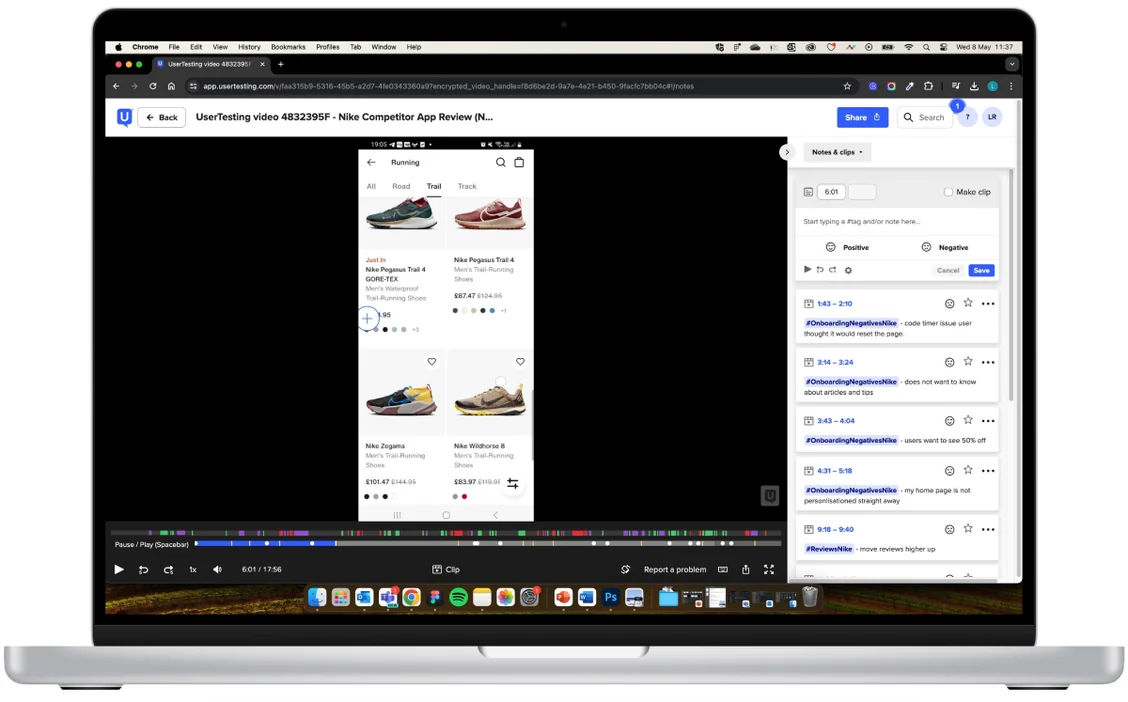

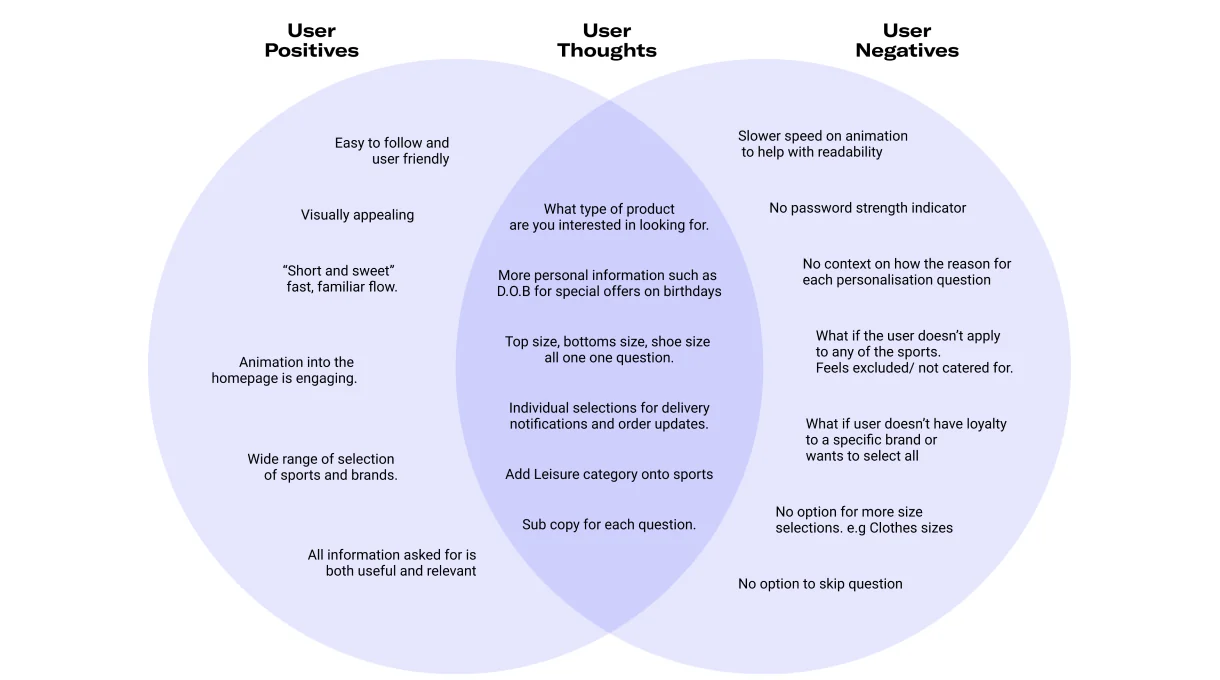

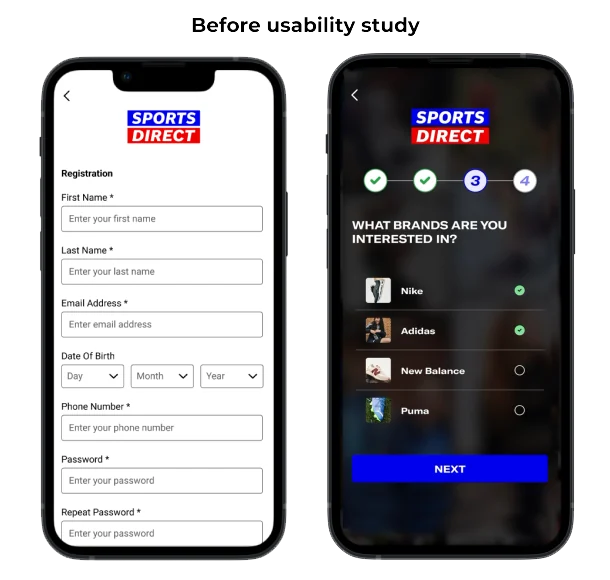

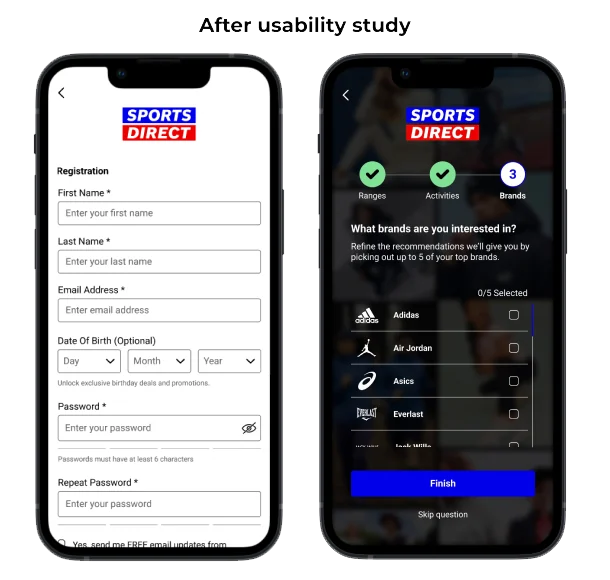

06 · Usability testing

I built a high-fidelity prototype and started with unmoderated testing, scripted so every participant hit the same moments. I wanted to know two things: could people get through it without help, and where were the usability and accessibility problems hiding. The findings drove a round of design changes, and retesting confirmed they’d worked.

Each design change traceable to a specific user insight.

The unmoderated rounds told me where people struggled. The moderated sessions told me why. Watching users navigate the prototype in real time meant I could chase the intent behind a hesitation, and validate each refinement before it was committed to build.

07 · Delivery

Once onboarding was handed over, my job widened. I established the design system and wrote product requirements alongside the developers. Sprint process came next, built to keep delivery honest week to week.

Sprint data from the feedback process introduced into the sprint framework.

08 · Outcomes

The work shipped. I left Frasers in August 2024, so the post-launch numbers sit with the business rather than with me, and I won’t quote figures I can’t stand behind. What I can point to is verifiable by anyone with a phone.

Shipped results and validated findings are real outcomes; signed-off targets are the goals the project was measured against, never presented as achieved unless confirmed.

09 · Reflection

The lessons I carried out of this project into how I lead design today.

Senior UX designer embedded in a live challenger bank. I took customers from sign-up to first transaction in a single session, down from a 3-5 day wait, and wrote the standard the team now works to with AI.

01 · The context

thinkmoney is a challenger bank with a clear purpose: helping people who struggle with traditional banking stay in control of their finances. The app is live and the users are real. Design decisions here have consequences for people who depend on the product to stay in control of their money.

I joined as Senior UX Designer, embedded in a cross-functional team alongside a Product Owner and developers. Unlike my previous roles, this isn’t building from scratch. It’s operating inside a mature product at pace: shipping while holding the standard, and thinking past the individual deliverable.

02 · Onboarding to first transaction

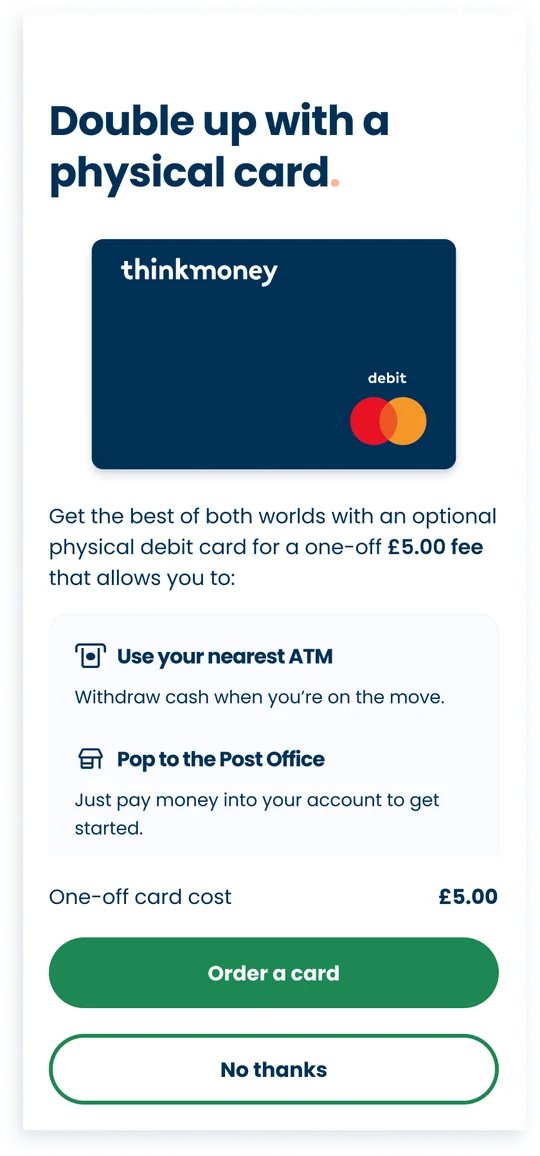

New thinkmoney customers waited three to five days for a physical card to arrive before they could transact. The card couldn’t simply be dropped: its delivery doubled as address verification. And the stakes ran deeper than convenience, because funding the account gates every downstream activation event. A customer who can’t fund can’t make a first payment, set up direct debits or upgrade.

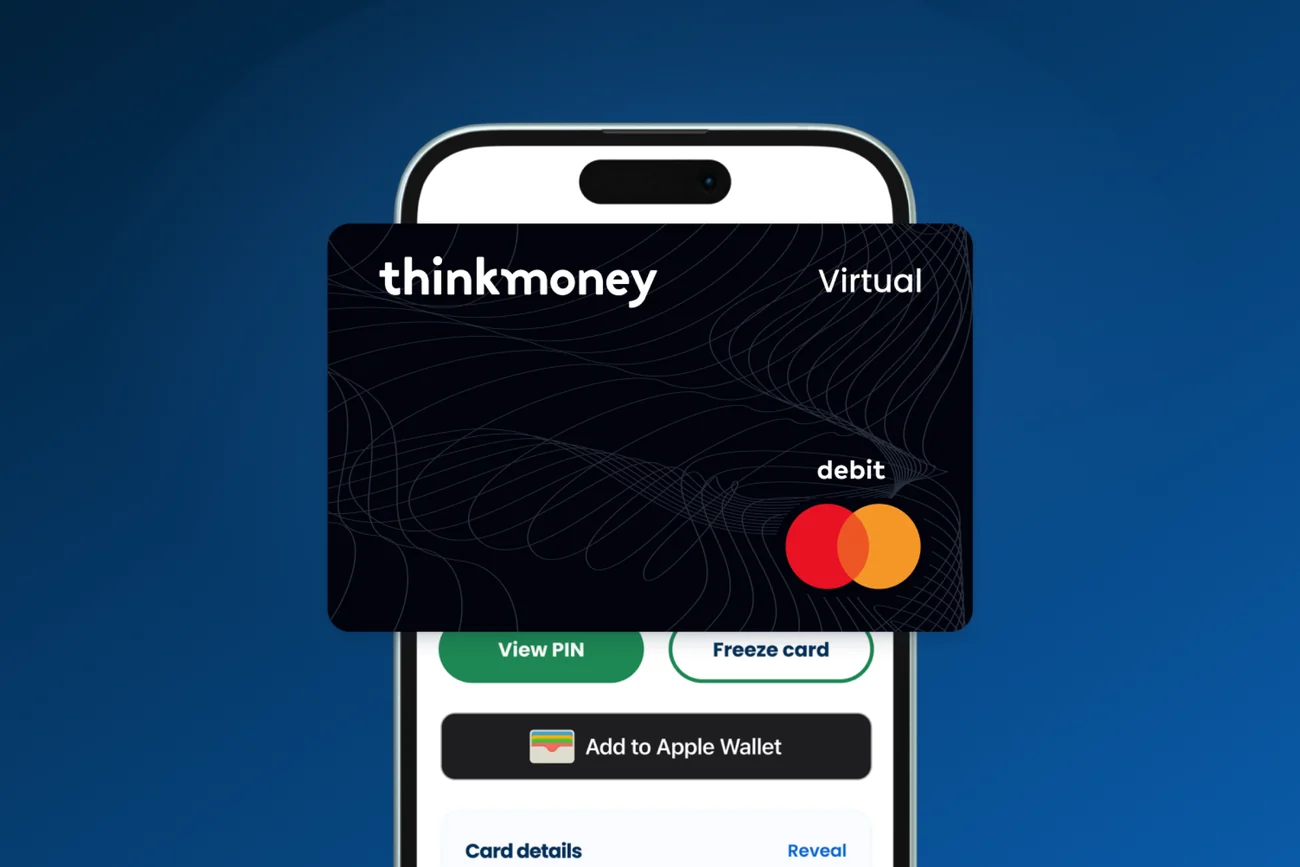

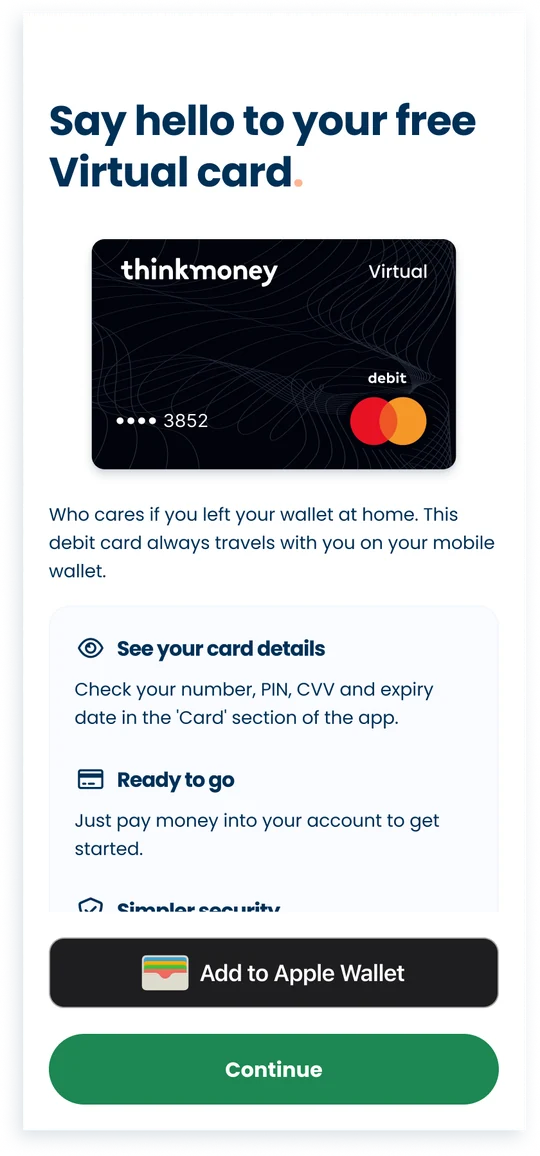

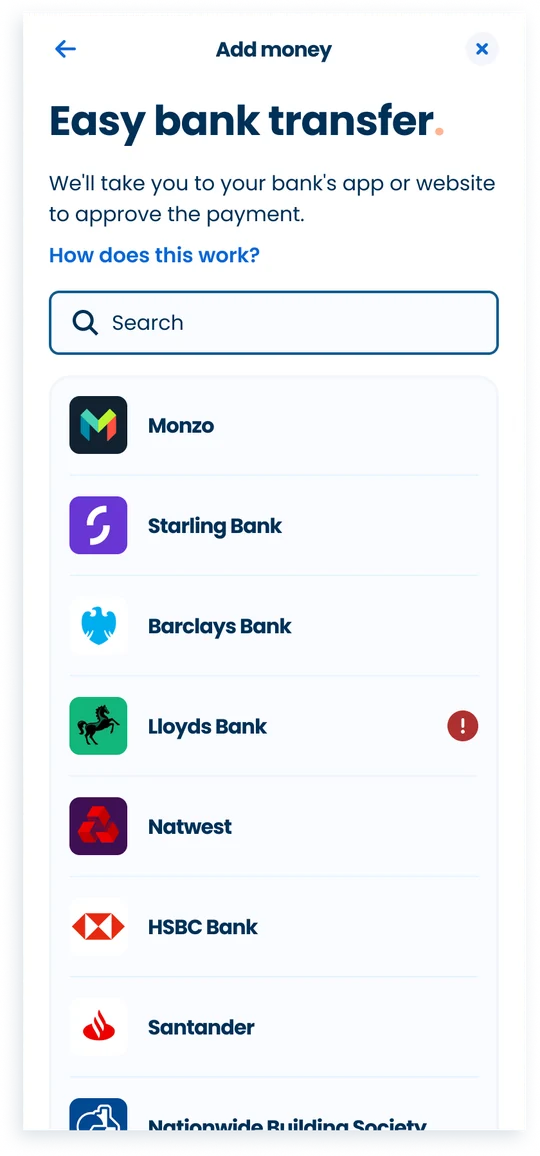

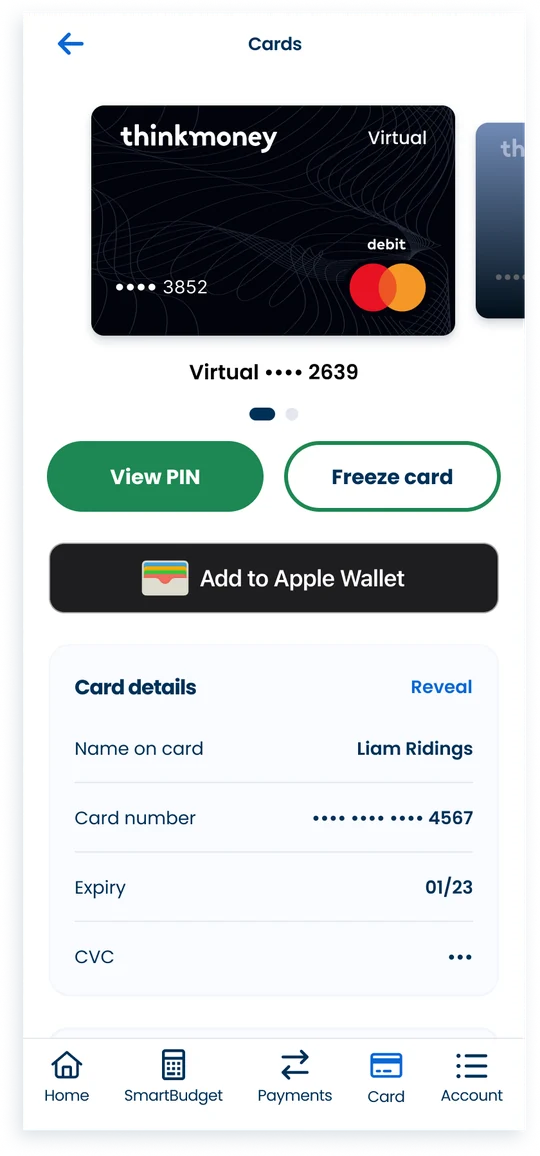

The answer was one continuous journey, not two features. I introduced virtual cards to the product for the first time and made them the default, with physical cards becoming opt-in. Then I designed the end-to-end Open Banking authorisation journey for account funding, scoped into the same onboarding flow, so a new customer funds by bank transfer in the session they sign up.

“Rather than leading with what the feature could do, I designed around the user’s real question: is this safe, and what do I actually get from it?”

That question shaped the funding flow in particular. Consent screens answer the unspoken concern before the user asks it, data sharing is stated plainly rather than in legal copy, and the benefit of connecting is visible upfront. The consent flow exists in service of funding the account, and it had to earn the trust of users who are already cautious about their money.

One session: card issued, account funded through Open Banking, first transaction possible before the customer closes the app.

Card management, still in design.

03 · First 30 days

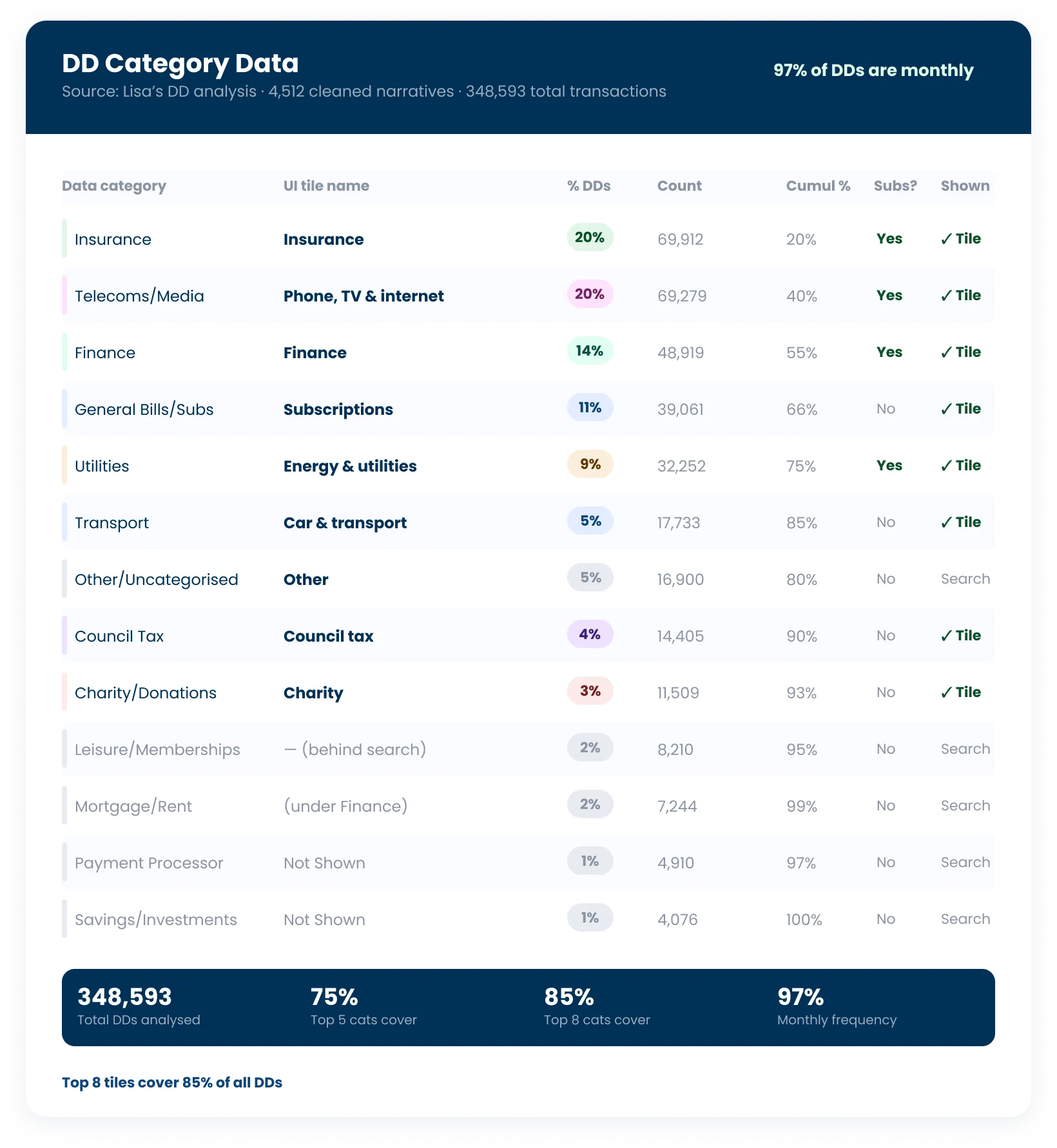

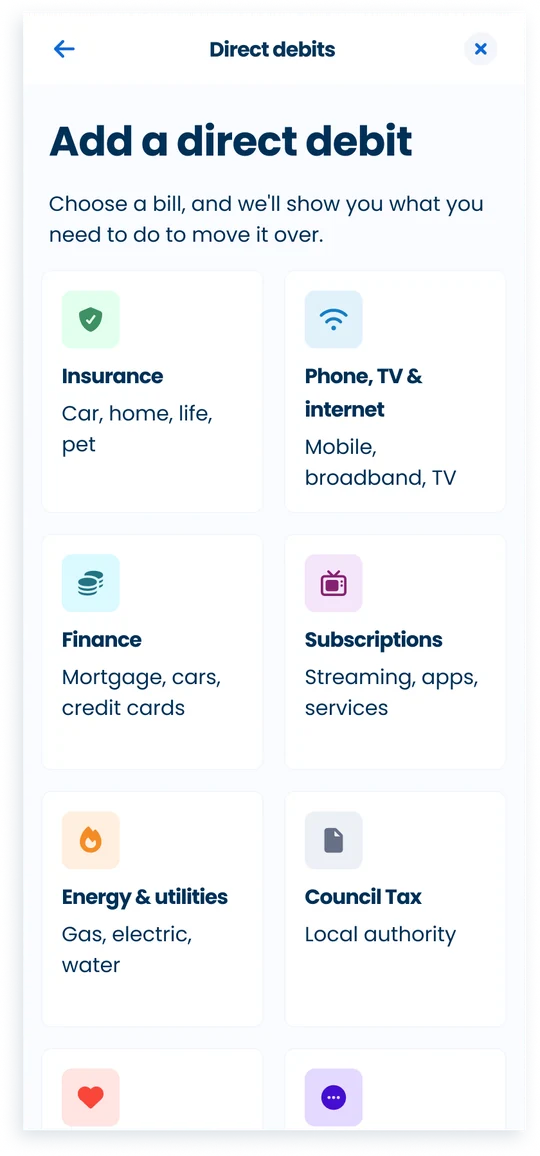

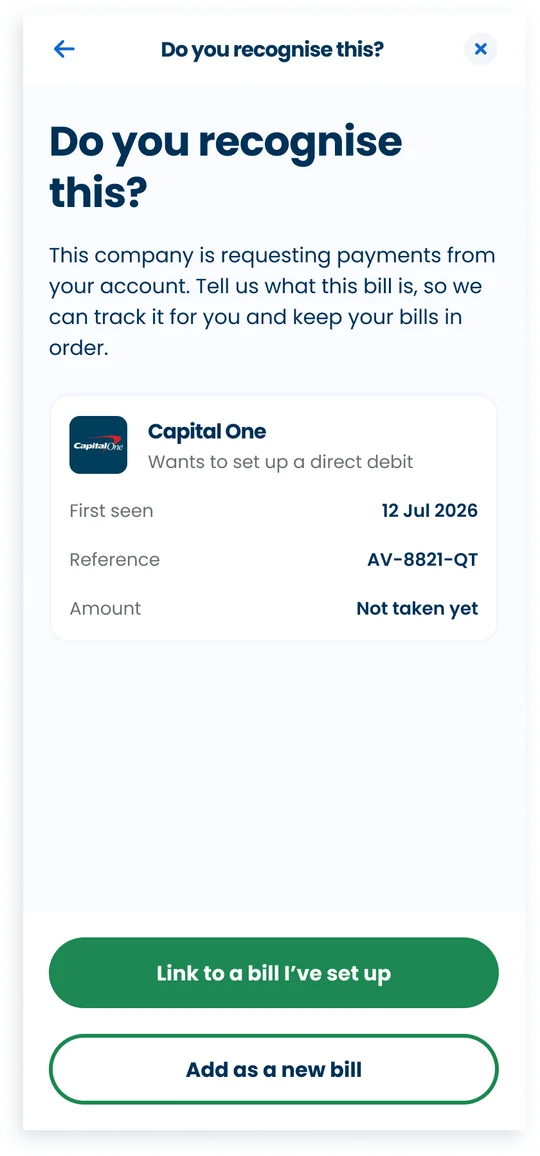

Funding solved, the next drop-off was plain to see: customers finished sign-up and landed on a home screen with nothing to do and no direction. Only 26% went on to set up direct debits unprompted, and direct debits are one of the strongest activation and retention signals the product has.

The detail I’d defend hardest: the direct debit categories weren’t chosen by intuition. Working from the analytics team’s analysis of 348,593 real direct debit transactions, I designed the tile hierarchy around what the data showed, so the eight tiles shown cover 85% of all direct debits and everything rarer sits behind search. The measurement plan was designed alongside the feature, not bolted on after it.

The category analysis behind the tiles: eight categories cover 85% of all direct debits, so those became tiles and the rest went behind search.

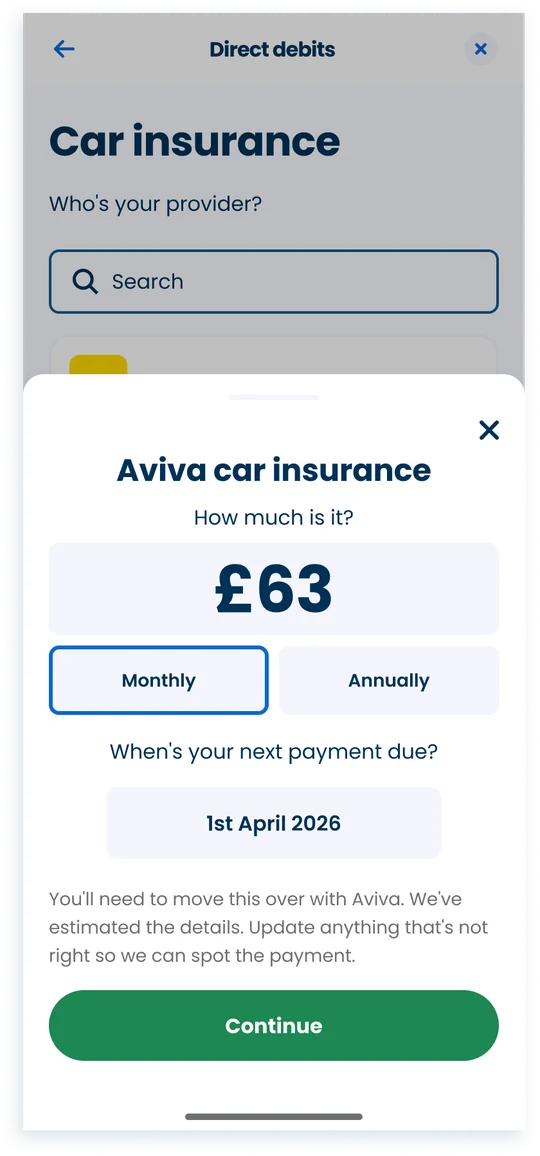

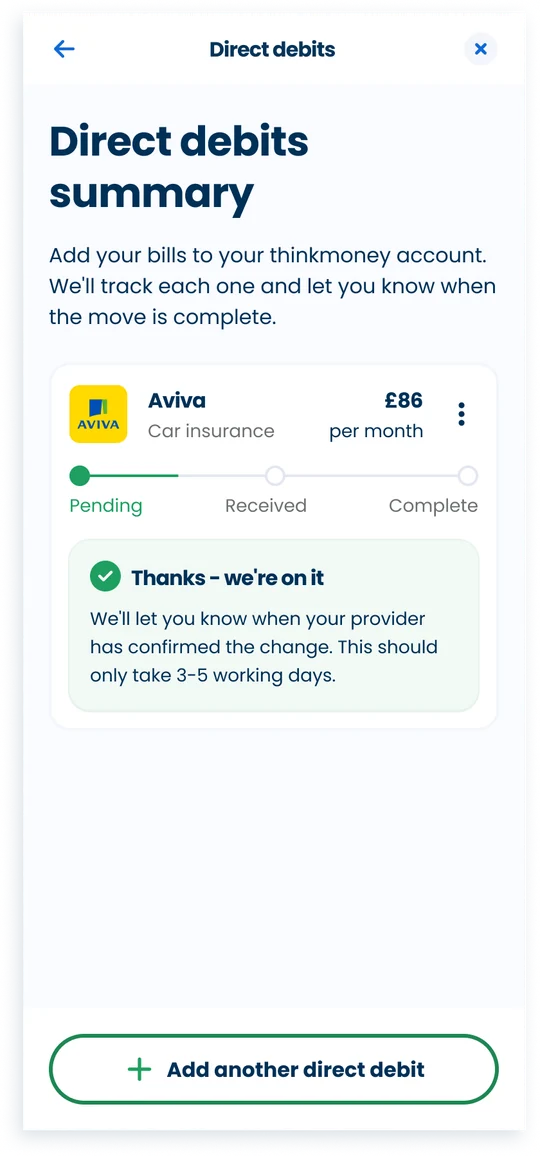

From that analysis, the end-to-end setup flow: choose a category, match the provider (including multi-bill providers like Aviva), then confirm and track.

Status: in design, go-live 31 July 2026. The concept and the direct debit first-prompt flow are approved by the CEO and Senior Product Lead.

04 · Design system

I maintain the thinkmoney design system across every product surface: the token architecture, the component library, and the build conventions the team works to. It is the reference point for design-engineering handoff.

Governance is deliberate. I sit on a three-person working group that controls what enters the system, with defined approval routes: new components and structural changes go to a weekly meeting, while minor variants and documentation updates run async via Teams with a two-working-day window. I also co-own the roadmap to an AI-queryable design system through Storybook.

Individual screens are the output. The system is what makes them coherent. Operating at both levels simultaneously is what distinguishes senior design work from executing features in isolation.

The system architecture, from primitives and tokens through to the components that ship on Figma, iOS and Android.

05 · AI in the workflow

I wrote “Claude × Design: Ways of Working”, the standard the UX team now works to. It defines Claude’s involvement at every phase of the process from discovery through delivery, from research planning and synthesis through wireframing, prototyping and testing to sign-off prep, dev handoff, QA and post-delivery documentation, with a named owner and a defined output for each.

The principles it sets are simple to state and hard to hold. Enable first. Protect design system integrity. Every team member benefits. Review AI output properly. And transparency always: any deliverable with a Claude contribution carries a visible note. The document also establishes the design system working group, its approval routes, and a seven-section documentation standard that every component entering the system is held to.

The part I’d point a sceptic at is the review checklist for AI-assisted output, built around the specific ways this work fails: confident but wrong, plausible but incomplete, tone drift, outdated context.

“Bringing AI into a design team isn’t really about the tool. It’s the same challenge as any UX work, understanding how people work, where the friction is, and designing a process that helps them do their best work more reliably.”

Designers who understand AI as a tool and can shape how it’s used in their teams are going to be significantly more effective over the next few years than those who don’t. Building that capability now, and doing it thoughtfully rather than reactively, is one of the most valuable things I can contribute to a team right now.

06 · Reflection

thinkmoney is a different kind of portfolio entry: no launch from zero, no greenfield freedom. What it shows is how I operate inside a live product, running parallel workstreams alongside POs and developers, holding quality at the system level, and paying attention to how the team works, not just what it ships.

The onboarding journey, the first-30-days work, the design system and the AI ways of working are all expressions of the same underlying approach: doing the work that needs doing, at whatever level it needs to happen.

About me

I’m a Senior UX Designer with experience across fintech, retail, and consumer products. I care about the full picture, research, strategy, systems, and craft, and I’m most at home in cross-functional teams where design has a real seat at the table.

I’ve led design on products used by millions of people, from the Sports Direct app to moneyappi, a financial wellbeing platform I helped build from the ground up as founding UX designer.

I’m particularly drawn to problems at the intersection of behaviour, technology, and trust, and I believe good design should change how people feel, not just what they can do.

Open to senior and lead UX roles, contract or permanent. If you’re working on something interesting, I’d love to hear about it.